RHA Blog

What Really Drives the Cost of Hydrogen Refueling Stations?

Author: Gildas Bonnier, Co-Founder, Grove Hydrogen Solutions

The price of hydrogen molecules matters. But for hydrogen stations, the larger challenge is utilization, uptime, and losses.

The high cost of dispensed hydrogen is usually explained in the simplest possible way: hydrogen molecules are expensive. That matters, but it does not explain the economics on its own. If the problem were only the price of hydrogen, the answer would be to find cheaper supply. But station costs are shaped just as much by throughput, reliability, and design choices. In California, station operators struggle to turn a profit even when retail hydrogen sells for around $35/kg and the cost of hydrogen itself accounts for only a small share of total station cost.

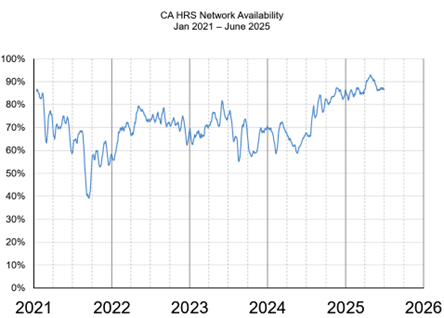

In a market still early in its commercial buildout, station economics depend not only on the price of hydrogen, but on station utilization, availability, and efficiency in turning delivered hydrogen into profitable throughput. In California, network uptime has struggled to exceed 85%. Some stations also lose a significant portion of the hydrogen delivered to them before it can be dispensed. And when stations are not sized properly for real demand, operators are left spreading a large fixed-cost base across too few kilograms sold. The result is a cost structure that is much more complex than a simple fuel-price narrative would suggest.

The usual way of looking at infrastructure costs does not fully capture this. Models rightly divide expenses into fixed and variable categories, but they do not clearly identify inefficiencies. Inefficiencies are typically buried inside fixed and variable cost line items rather than treated as their own driver of station economics. Fixed costs include site preparation, permitting, lease expense, capital recovery, and operations and maintenance. Variable costs include hydrogen and utilities. It is also useful to isolate a third bucket: inefficiencies, including missed sales from downtime, extra operating burden, and hydrogen losses, even though those costs are often embedded within fixed and variable line items. For hydrogen stations, that bucket is not incidental; it is a major cost driver.

For clarity, the following figures do not include state incentives such as California’s Hydrogen Refueling Infrastructure (HRI) program and Low Carbon Fuel Standard (LCFS). The HRI program offsets part of the capital recovery cost by generating revenue for unused capacity, but because it is also tied to station uptime, it increases the economic impact of unreliability.

That is why operations and maintenance look different in hydrogen than it does in more mature industries. In a conventional business, O&M usually means safety oversight, technicians, spare parts, and service schedules. In hydrogen, it also means reliability support, process support, supplier management, and continuous improvement with vendors. Operators are not just maintaining equipment. They are dealing with the commercial consequences of a technology that still demands significant support around it.

A case involving a liquid-hydrogen mobile fueler serving heavy-duty trucks in Southern California illustrates this. On paper, the model sounds simple: hydrogen supply, mobile fueling equipment, and staffing, when in reality, it required much more.

Demand was concentrated in specific windows, and the site had to support clustered fueling and high-pressure service for trucks. Deployment speed mattered. Reliability mattered even more, because the station was supporting truck deployments and vehicle sales. A station outage was not just inconvenient, it had immediate operating consequences for truck owners.

That shaped the operating model from the start. The site used two mobile fueling assets instead of one for redundancy. It required site-level operating coverage to deal with issues as they arose, technical support focused on reliability and efficiency, and active coordination with suppliers. With that operating model, the site supported near-100% availability. That technical support tracked reliability events, identified root causes, worked with vendors to prevent recurrence, and used station data to anticipate failures and schedule maintenance to preserve availability. In practice, equipment cost and fuel cost alone do not capture what commercially usable infrastructure requires, even for temporary solutions.

The long-term goal is not to carry a heavy operating model forever. It is to improve reliability enough that stations can run at very high uptime with less redundancy, lighter field operations, and lower support overhead.

The supply chain is part of the same challenge. Cost and reliability depend not only on station equipment, but also on local supply availability, backup sources, and delivery logistics, whether through onsite production or gaseous or liquid supply chains. No station can be more reliable than the hydrogen supply chain behind it. Even commercial terms affect long-term flexibility, cost, and resilience.

There is no single best hydrogen station design. What works best depends on the use case. The right sequence is to start with demand, then assess reliability needs, then examine hydrogen sourcing realities, and only after that choose the technology. Too often, future station owners do the reverse: they start with a preferred technical configuration and then try to fit the use case around it, leading to operational and economic mismatches.

Improved uptime, lower losses, and better alignment between station design and demand profiles will do nearly as much to lower costs as cheaper hydrogen itself. Lower-cost hydrogen matters. But for hydrogen mobility to scale, stations also have to work.